October 28-29, 2008

Relaxing on Koh Phangan

Much as I like Penang, I’m happy to be away from the bustle and noise of Georgetown for a while. I woke this morning to the sound of gentle rain hitting the roof of my seaside bungalow in Koh Phangan. With my Malaysian visa about to expire, I took it as an opportunity to visit Thailand again, choosing to return to the island (koh) that I visited last year. Koh Phangan in comparison to its better-known near neighbor, Koh Samui, is still relatively unspoiled. Although tourism is its economic base, it has not yet been overbuilt and overrun by upscale resorts and high rise condos. There is still a lot of open space and the typical accommodations consist of modest bungalows strung out along the various beaches.

A major attraction of Koh Phangan is the “full moon party” that attracts the twenty-something party crowd. I guess it was inevitable that ambitious entrepreneurs would augment that attraction by staging “half-moon” and “dark moon parties,” as well. Fortunately, that scene is easily avoided as it happens mainly at the south end of the island near Had Rin. The remainder of the island offers various levels of peace and quiet, nice beaches and clean water. Expenses are a bit higher here than in Penang but still affordable. I’m sure I could find ways to economize if I were to commit to a longer stay. It’s off season now so it’s a buyer’s market for lodgings. I dare say that ninety percent of the units are vacant right now.

The only sizeable village on the island is Thong Sala, located on the western side. That’s where the ferry docks are. It has all the usual conveniences – shops, restaurants, banks, cafes, and a nice night market where one can get a good cheap meal. I prefer to stay to the north and not too far away from Thong Sala at one of the many bungalow places that line the shore. The place I’m at is fairly new and clean and has screened windows, a rarity in these parts. It has no A/C, only a fan, but that’s quite adequate as it doesn’t get too hot here and there’s usually a breeze off the ocean.

The antipode to the party scene is the yoga/health spa scene. There is a sizeable cluster of people who come to the island for yoga workshops, personal growth, healing, and spiritual development. I first learned about Koh Phangan from my Italian friend, Michele, whom I met at Auroville last year. He had come here earlier that year to do yoga at the popular Agama Center which has a loose affiliation with the Ananda Yoga Resort where one can find various health oriented offerings like vegetarian food, yoga classes, sauna, massage, and a seven day colon cleanse program.

I came to the island last year prior to my visit to Bali. I liked it but was able to stay for only two weeks. Michele was not on the island at that time so I had to discover it on my own. This time, he is here so I have the advantage of being guided and introduced to people by someone who has spent a lot of time here.

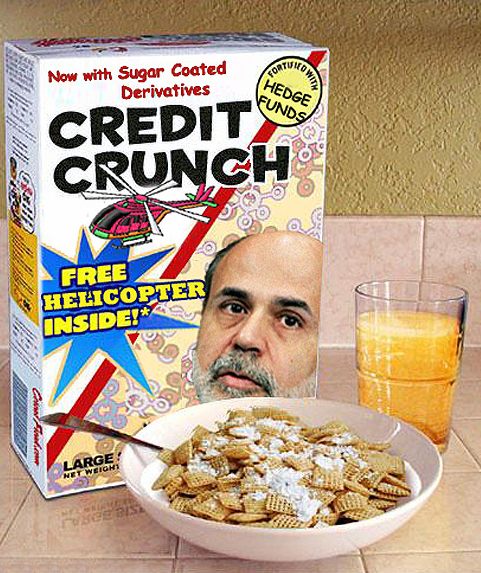

The Bank Bailout Scam

What can you expect when a fox is appointed to manage the hen house? Our current Treasury secretary, Henry Paulson, was formerly the CEO of Goldman Sachs, one of the most powerful financial institutions in the world. His appointment to that post was clearly intended to enable a continuation of the long trend of greater concentration of power and wealth in elite hands.

Recent moves by the U.S. Treasury make that ever more obvious. In an article in Saturday’s (Oct. 25) New York Times, Times economic columnist, Joe Nocera, reveals what he calls “the dirty little secret of the banking industry”–namely, that “it has no intention of using the [government bailout] money to make new loans.”

Nocera explains that the Paulson plan to hand over $250 billion [in money borrowed into existence by the government] to the biggest banks, in exchange for non-voting stock, was never really intended to get them to resume lending to businesses and consumers, as was stated. That was just window dressing. The real purpose of the bailout is to engineer a rapid consolidation of the banking industry by enabling at public expense a wave of takeovers of smaller financial firms by the most powerful privileged banks. Examples, so far:

JPMorgan’s recent government-backed acquisition of two large competitors, Bear Stearns and Washington Mutual; the takeover of Merrill Lynch by Bank of America, Wachovia by Wells Fargo and, National City by PNC.

There’s more to come, and by deciding which banks get handouts and which don’t the entire consolidation process is being orchestrated from the top.

Expatriate Living

An “expatriate” is one who lives outside of his/her homeland. That term should not be confused with “ex-patriot,” who is someone who once was patriotic but is no longer. Not that the two are mutually exclusive, of course, but let’s not go off on that tangent just now. The “expat” lifestyle suits me very well. Besides enabling me to stretch the purchasing power of my small pension, there are social, educational, cultural, and even spiritual benefits to living abroad. That’s especially true when one gets away from the areas that are dependent upon tourism and immerses oneself for extended periods of time in the daily routines of ordinary people, which is something I feel I’ve barely started to do. It has been said that “travel broadens on,” but I would venture to say that living abroad tends to make one less nationalistic, more humanistic, and more appreciative of the things that all people have in common.

Communicating

When I left the U.S., I suspended my Verizon cell phone account. Their rates for international service are quite unreasonable in comparison to what’s available in Asia. Mobile phone dealers are everywhere here and the competition is fierce, so some phones and most services can be had pretty cheaply. The common practice here is to buy your own phone then buy a SIM card from one of the many service providers, then buy minutes of call time. As I understand it, you pay only for outgoing calls, not incoming, but there is an expiration date on your outgoing call time the duration of which depends on how big a block of time you buy. In Malaysia ten Ringgit was good for ten days, thirty Ringgit for thirty days.

Cheap as it is in Malaysia, service in Thailand seems even cheaper. To avoid high roaming charges on my Malaysian service, I did as I was advised by other travelers and bought another SIM card when I got to Hat Yai, my first stop in Thailand. The SIM card is a tiny electronic chip that slips into a slot just beneath the phone’s battery. Anyone can install it in about ten seconds. People at my guest house directed me to a shop right next door where I paid 50 baht (about $1.50) for a SIM card. I then “topped-up” my card at the guest house with 100 baht worth of call time. At .80 baht per minute that gave me 125 minutes of domestic call time, good until December 2. At a total cost of less than 5 dollars that’s not bad. No wonder every teenage kid in Asia has a mobile phone. Oh, and I can call internationally, too, (including the U.S.) at somewhat higher but still cheap rates. If the FCC was really doing its job, we’d have similarly good, cheap, mobile service in the U.S.

In Asia, people tend to use SMS (short message system) or text messaging more than voice communication. My own usage has changed accordingly. Text messages provide a much more accurate way of communicating, can be saved in phone memory, and are very inexpensive. I have my phone set to automatically save both incoming and outgoing messages, then I occasionally delete those that I no longer need. I hardly ever make a voice call anymore.

Sicko

DVD’s of popular movies, which are surely pirated, are sold openly at very low prices in Malaysia, Thailand, India, China, and I’m sure, other parts of Asia. A couple weeks ago I picked up a few for 5 Ringgit (US$1.60) each. Among them was Michael Moore’s latest film, Sicko. It is in my opinion his best yet, and I urge everyone to see it. The film provides a clear description of the appalling state of the American “health care” system and compares it with systems in Canada, the UK, France and Cuba. If those countries are able to provide good, free health care for their people, The US should be able to do it too.

State of Fear

Browsing the small collection of books available at my resort, I came across Michael Crichton’s, State of Fear. Reportedly a bestseller, it looked to be the most interesting amongst the available titles (aside from the two copies of Tolstoy’s War and Peace). It did not at first register with my conscious mind, but I was reminded a few days later, when I recommended it to him, that Peter Etherden, my good friend and colleague in the UK, had urged me a few years ago to read this book. Coincidence? Following my recommendation to him, Peter came back with: “I have been trying to persuade colleagues to read State of Fear since it first came out in 2004…when I found to my surprise that all the references in the extensive endnotes checked out. Prior to reading it I had believed the environmentalists’ case without looking into the data and the premises behind their claims.”

In this book, Crichton tells a whale of a tale. It’s quite engaging fiction, but it’s also designed to inform, just, as, Peter notes, was much of Charles Dickens’s work. In this case, the bad guys are money grubbing con men who have control over a major environmental organization. The plot revolves around the good guys and gals who attempt to foil the heinous criminal plans of the con men to create major disasters that can be blamed on human-induced climate change. These are crimes that are intended to pump up the “state of fear,” which is the underlying theme of the book. One of Crichton’s main characters argues, rather convincingly, that the global warming theory is not well supported by the actual scientific evidence, which Crichton provides for the reader in abundance.

When Peter first began expressing his doubts a few years ago about the global warming theory I thought he had gone over to the dark side because by then everybody “knew” that global warming was an irrefutable fact. Now, with the widespread viewing of Al Gore’s polemical film, An Inconvenient Truth, that “fact” is even more firmly entrenched in the public mind. I personally was an early believer in the global warming effect of the buildup of greenhouse gases (mainly carbon dioxide) and the prospect of abrupt climate change. That belief was based on my 1982 reading of John Hamaker’s book, The Survival of Civilization. Hamaker argued that this was a natural cycle with a period of about one hundred thousand years. He said it might be exacerbated by human activities, but was essentially quite independent of them. Hamaker’s evidence was paleontological, based on the physical examination of glacial ice cores and fossils.

His prediction was that the greenhouse effect would lead to more turbulent weather patterns in the temperate zones and eventually bring on another ice age. That seemingly paradoxical prediction was explained as follows:

More solar energy trapped in the atmosphere causes greater amounts of water to be evaporated from the oceans and lakes; this vapor causes greater cloud cover which migrates toward the poles covering more of the polar and temperate zones, blocking the sun’s energy and causing cooling in those regions. The result is greater wind shear – storms, tornados and hurricanes at the interface between the tropics and the temperate zones, and ultimately, global cooling and glaciation. And what drives this process of CO2 buildup in the first place? The depletion of minerals in the surface soils which cause plant growth to be less intense. And how does glaciation correct that? By bringing new minerals to the surface, which stimulates new plant growth, which takes more CO2 out of the atmosphere, which reverses the greenhouse effect, which causes the glaciers to recede. Hamaker’s prescription for ameliorating the effects of those changes – remineralize the soil by grinding up rocks (glacial till) and spreading the dust over fields and forests.

Well, it sort of made sense to me, though I did not dig very deeply into the subject. Subsequent studies by mainstream scientists, we are being told, confirm the CO2 buildup and the global warming phenomenon. The CO2 figures cited by Crichton confirm the buildup showing an increase from 316 parts per million in 1958 to 376 ppm in 2002. That’s an increase of 60 ppm or about 19 percent in 45 years. Crichton’s character minimizes the importance of that amount of change, but I find the argument less than compelling. Hamaker argued that the rate of CO2 increase is exponential (changing at an accelerating rate) not linear (changing at a constant rate), something that doesn’t show up in the limited data provided by Crichton. As for the global warming effect, Crichton argues against it by showing that, while some places have gotten warmer, others have actually gotten cooler. But if Hamaker’s thesis is correct, that is to be expected. It begs the question, is there a locational pattern to the places that have gotten cooler, and what are the geographical and weather variables that might explain that pattern?

Well, I don’t know, maybe we have global warming, maybe global cooling, maybe climate change, maybe not, but one thing seems clear – we’ve been making a mess of our planet with deforestation, urban sprawl, and pollution of many kinds that makes living in many places quite unpleasant or even downright dangerous. We ought to do something about that. But let’s get back to the main theme – fear. Is there a conspiracy to make us ever more fearful? Conspiracies abound, but anyone who tries to reveal the evidence of them is ridiculed and lumped into the category of paranoid nut cases. But there will always be wolves in sheep’s clothing and foxes getting into hen houses, who all the time try to tell us “There ain’t nobody here but us chickens.”

Crichton’s own “nutty professor” argues in the book that starting in 1989 there was a “major shift” in the media’s use of terms like crisis, catastrophe, plague, disaster, dire, unprecedented, and dreaded, and that it was all deliberate hype because “politicians need fears to control the population.” With the collapse of the “Communist menace,” a whole string of other threats have been trotted out as replacements. Whether it is real or imagined, climate change is one of them.

Power politics is no more than a big protection racket. As H. L. Mencken observed more than 70 years ago, “The whole art of practical politics is to keep the populace alarmed, and hence clamorous to be led to safety, by menacing it with an endless series of hobgoblins – all of them imaginary.” The power elite will always pose as our saviors, offering new plans and programs that they say will protect us or save us. They tell us there is no alternative (TINA). It’s time we started cooperating to create alternatives that reflect our own values and ideals and promote the common good. Remember the words of President Franklin Roosevelt: “We have nothing to fear but fear itself.”

{kind=link}