In 2013 I wrote an article that was published in the online academic journal, Internet Journal of Community Currency Research (IJCCR). That article, Taking Moneyless Exchange to Scale: Measuring and Maintaining the Health of a Credit Clearing System, was intended to bring order out of the chaos that prevailed within the movement to create decentralized moneyless systems of reciprocal exchange based on the credit clearing process.

Alas, that article attracted little notice and stimulated no significant action to correct common errors and improve system operations. But this matter is far too important to leave it at that. Fortunately, the past few years have seen the development and deployment of some powerful new communication tools that are able to create high quality, short audio and video overviews that make concepts and prescriptions accessible to anyone.

Over the past several weeks I have been making extensive use of these tools with amazing results and posting the output on my website, https://beyondmoney.net/, and elsewhere; I am doing the same in this case. is a 7 minute video overview of the article:

And here is a longer, more comprehensive 14 minute audio overview.

If you have any interest at all in reclaiming the “credit commons,” participating in decentralized, community-controlled exchange alternatives, and transcending the destructive political money regime, these are essential to understanding how to move forward.

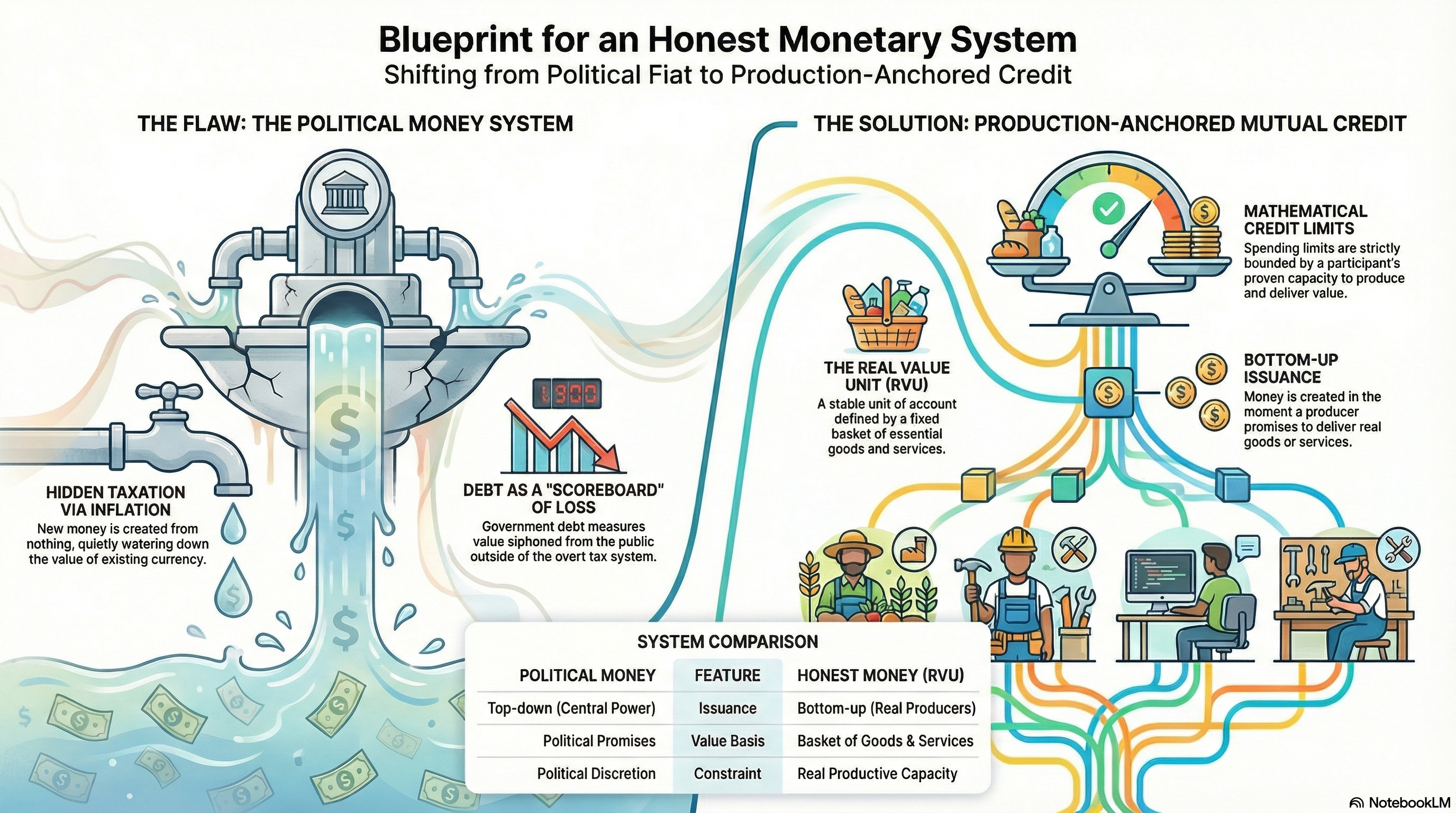

I recently had a conversation with Copilot about designing an honest and effective exchange system that would circumvent the flawed and exploitative fiat money system. I began by saying, “The political money system is structurally flawed, and its eventual collapse is inevitable. That may occur slowly over time via inflation or suddenly with a declared devaluation; in either case the users of the currency suffer losses. Government debt is merely a measure of how much value has been taken from the people outside of the overt tax system. Let’s design an honest monetary system where issuance cannot outrun real output of goods and services.”

That conversation was built around my writings which were fed into Copilot and my responses to Copilot’s replies over several rounds. I then uploaded that entire conversation to Google’s NotebookLM and asked it to generate a video overview that puts it all into a concise non-mathematical description of what I’m aiming to build? The video it produced is truly awesome in explaining, in terms that virtually anyone can understand, how an honest and effective decentralized money system that is anchored to the real economy can be structured and how it operates.

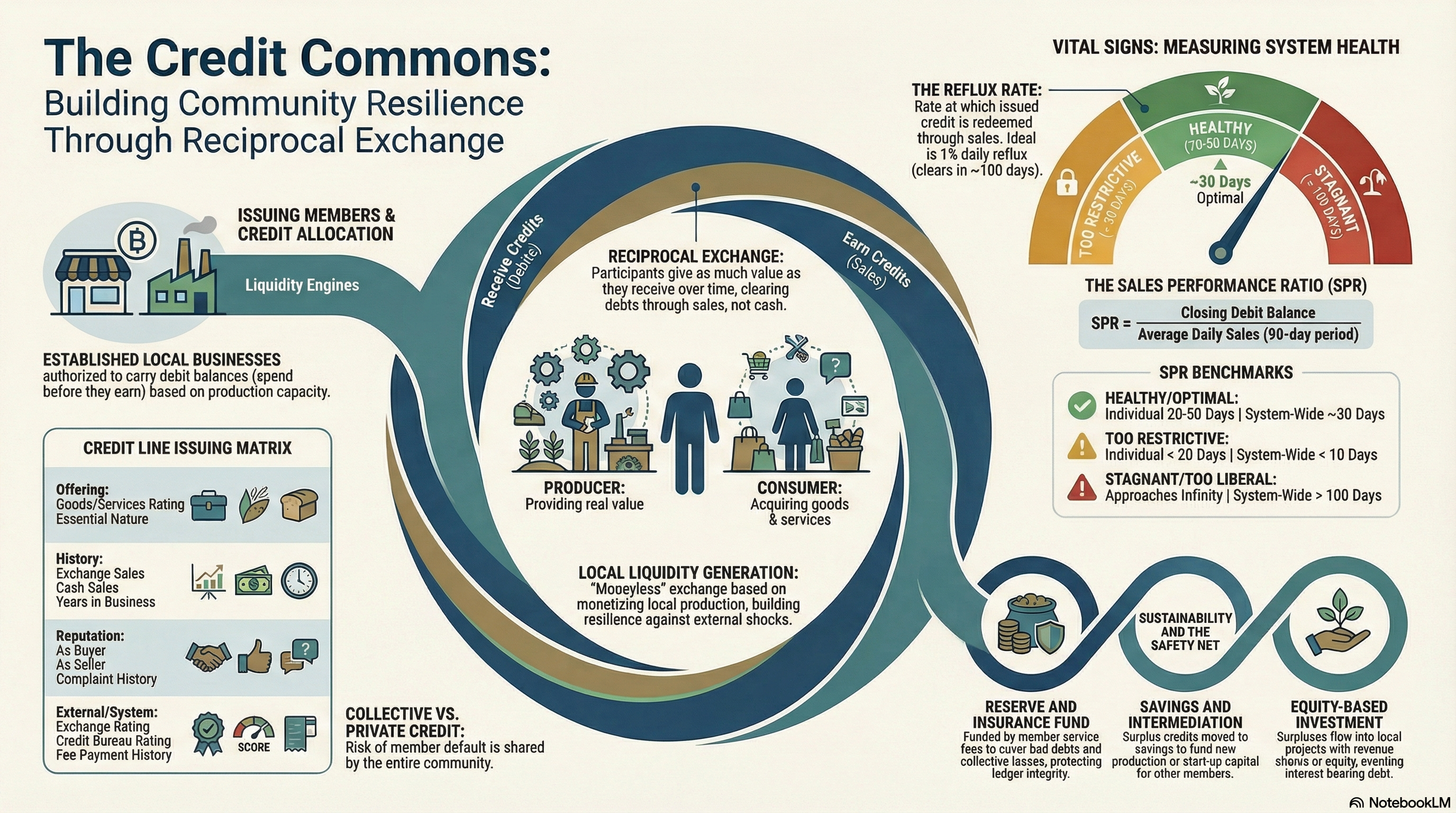

It has long been my position that a real alternative to fiat money as a means of payment requires reclaiming the “credit commons,” i.e. establishing community control over credit. It is producers and sellers of real value who are the ones who are actually qualified to issue a currency into circulation. They can do so individually by using their own private voucher currencies redeemable for the goods and services they are ready, willing, and able to provide, or they can do it in cooperation with others by pooling their commitments and jointly issuing a common voucher currency. Such a currency can then circulate generally for other to use to pay one another instead of using dollars. Euros, pounds, or other government fiat currencies.

My paper titled, Invoice Factoring as the Basis for a Digital Token Currency, presented at the RAMICS Conference in Rome on November 6, 2024, describes how that can be achieved by creating a digital token currency that, unlike present-day crypto currencies, is based on, and redeemable for real goods and services. This presentation describes the structure, processes, and protocols for creating and circulating a digital voucher token currency on a continuous recurrent basis. I’ve summarized my proposal in this 12-minute video posted on YouTube.

Chapter 16 is the latest Chapter in my new updated and expanded edition of The End of Money and the Future of Civilization. The link to this chapter is now listed along with the other previously published chapters on the book page along with links to the audio narrations by Ken Richings. Scroll down to find Chapter 16 there or click here to go directly to the PDF file.

Here are the Chapter contents:

Figure 16.1 A Typical Small Boat Harbor (Drawing by Dennis Pacheco)

The Orthodox Approach to Community Economic Development

A Comprehensive Community Economic Development Plan

Stage I: Map the Local Actors and Assets & Promote Import Substitution

Stage II: Support Structures for Localization—Saving, Investment, Finance, and Education

Stage III: New Liquidity Through Trust—Mutual Credit as a Way to Pay How It Works Key Benefits The Generation and Allocation of Trade Credits

Stage IV: The Credit of “Trusted Issuers” Can Provide a Local Alternative Currency for General Circulation

Stage V and Beyond: Transition to an Objective Measure of Value and Unit of Account

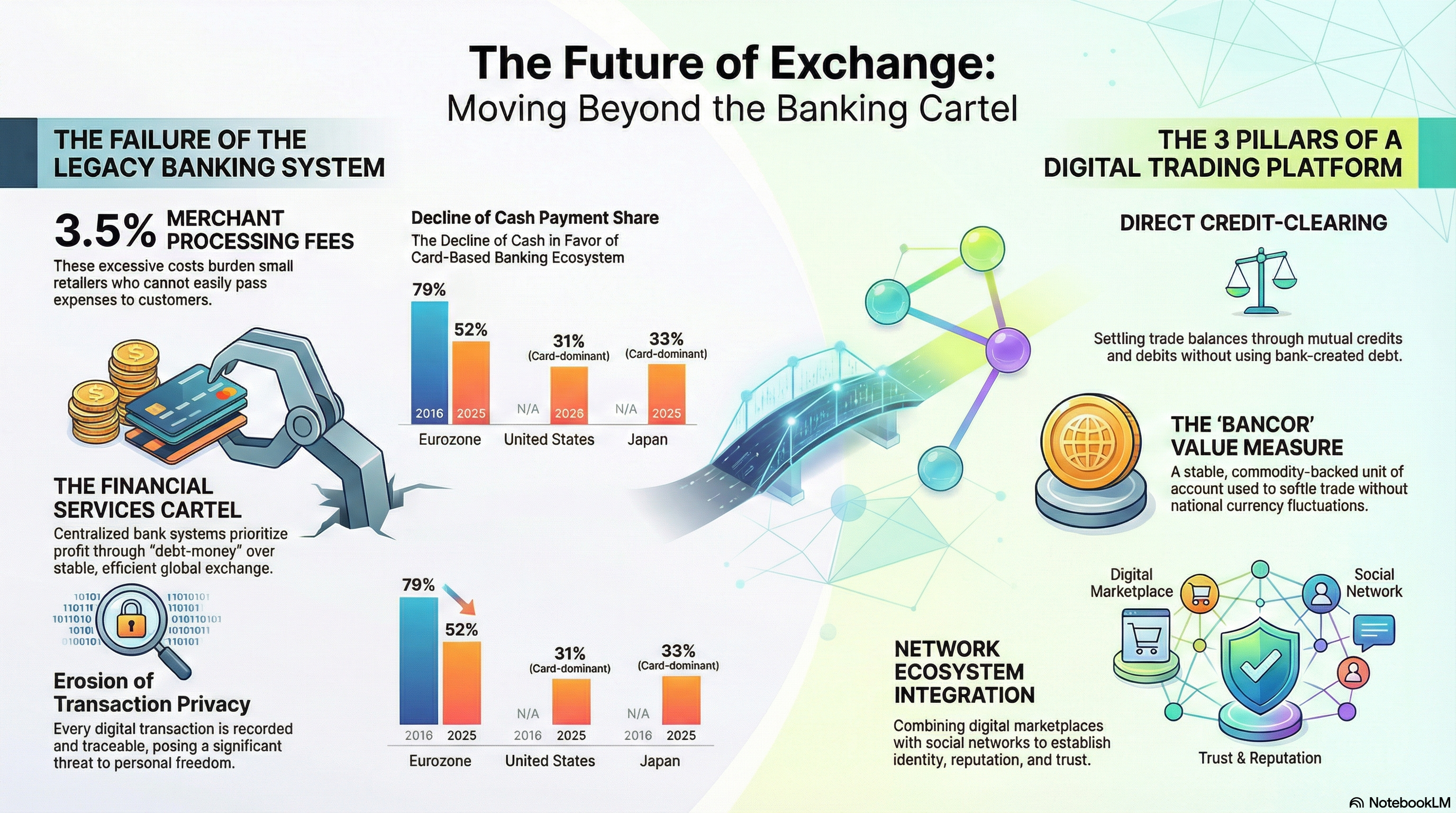

If the BRICS ever hope to escape the orbit and dominance of the Western Empire they will need to organize an international clearing Union under their own control, along the lines of the Bancor proposal of John Maynard Keynes which he put forth in 1944 at the Bretton Woods conference. If that proposal had been adopted it might have saved the world 80 years of grief and violent conflict.

Further pertinent information from Alistaire Crooke

Today, out of curiosity, I asked Copilot this question:

“How would E. C. Riegel organize the exchange of value among producers and intermediaries in the distribution process?”

Here is Copilots’ surprisingly accurate response to that question. It is, in effect, a brief summary of his book Private Enterprise Money.

E. C. Riegel envisioned a radically decentralized and voluntary system of value exchange that bypassed both government-issued money and centralized banking. His proposed framework, known as the Valun Exchange System, was designed to empower producers and intermediaries to coordinate trade through a self-regulated, non-political monetary mechanism.

Here’s how it would work in practice:

1. Voluntary Association of Producers: Producers and intermediaries would form a cooperative network called a Valun Exchange. Membership would be voluntary and based on mutual trust and creditworthiness.

2. Private Credit as Currency: Instead of using state-issued money, members would issue credit to one another in the form of Valun units. These units would be backed by the members’ productive capacity and promises to deliver goods or services—not by gold, fiat, or government decree.

3. Accounts, Not Cash: Transactions would be recorded as debits and credits in members’ accounts, similar to a mutual credit system. No physical currency would be needed; the system would operate through bookkeeping entries.

4. Intermediaries as Facilitators: Distributors, wholesalers, and retailers would participate as both buyers and sellers, using their Valun accounts to settle transactions. Their role would be to facilitate the flow of goods, not to extract value through speculative finance.

5. Self-Limiting Credit: A member’s ability to issue credit would be limited by their past performance and the confidence of the network. This would prevent inflation and ensure that credit was grounded in real economic activity.

6. No Interest, No Taxes: Since the system was private and voluntary, it would not involve interest-bearing loans or taxation. Riegel believed this would eliminate many distortions in the traditional monetary system.

In essence, Riegel’s model treated money not as a commodity or a government tool, but as a social contract among producers—a means of measuring and facilitating exchange based on trust and productivity. It was a bold attempt to return the power of money creation to the people actually producing value.

If you’d like, I can sketch out a visual flow of how this system would operate among producers, intermediaries, and consumers.

To that offer, I answered, “yes,” but in successive attempts Copilot failed to produce an accurate flow diagram. I have for many years been using my own diagram of credit flows in mutual credit clearing systems. Here it is below. If you substitute the word “valun” for “Currency vouchers,” this diagram shows exactly what Riegel was describing:

The “Trusted Producer” depicted in the upper right begins the process by using their line of credit to purchase something for an employee, supplier or contractor. Those credit vouchers then flow in the numbered sequence, the final step being when the Trusted Issuer accepts them back in payment for the goods or services they sell, thus completing the circuit of reciprocity. Note that at each step of the way, goods and services are circulating in the opposite direction to the voucher credits (or valuns).

I then pointed out to Copilot that it had failed to specify the units in which valun credits were to be denominated. This was its response:

Great point, Thomas. Riegel proposed that all debits and credits in his system would be denominated in a unit called the Valun—short for “value unit”. This was not just a name, but a deliberate attempt to establish a new standard of value independent of national currencies and political influence.

At the system’s launch, the Valun was intended to be roughly equivalent in purchasing power to the U.S. dollar, simply to ease adoption and pricing familiarity. However, over time, its value would be maintained internally by the productivity and trustworthiness of the network’s members, not by fiat or commodity backing.

So, in essence, every transaction—whether between producers, intermediaries, or consumers—would be recorded in Valuns, making it a closed-loop accounting system grounded in mutual credit and real economic activity.

Would you like a breakdown of how Valun pricing might work in practice, or how it could be stabilized over time?

I already knew how Riegel proposed to stabilize the Valun pricing unit, and I am not satisfied with it being adequate. I make my case in a document which Copilot cited as a source; it is contained in a previous post to my website, E. C. Riegel’s Valun Mutual Money Plan, but the reference was to a site other than my own. It would be better to read the original post on my site. That post contains the full text of the Valun Mutual Money Plan, together with my comments and critique. I believe that serious students would do well to read it.

Chapter 15 is the latest Chapter in my new updated and expanded edition of The End of Money and the Future of Civilization. The link to this chapter is now listed along with the other previously published chapters on the book page along with links to the audio narrations by Ken Richings. Scroll down to find Chapter 15 there or click here to go directly to the PDF file.

This is the latest chapter to be published of my new 2024 edition of The End of Money and the Future of Civilization. It continues the exposition begun in Chapter 13, elaborating upon sound principles of credit allocation and management, highlighting what did not work and why, and describing in detail what it takes to make an exchange alternative succeed. It answers crucial questions like:

Who Is Qualified to Issue Currency?

On What Basis Should Currency Be Issued?

How Much Currency May Be Issued?

How to Determine the Period of validity?

And considers strategies for successful launch and implementaion, with due regard for the broad situational context into which an alternative currency or credit clearing exchange may be introduced.

The first edition of my book, The End of Money and the Future of Civilization, was published by Chelsea Green Publishing in 2009. While it remains as relevant today as it was when first published the printed book has been out of print for several years. But, having had the rights reverted to me by my publisher, I am making the entire book available for free in PDF format. You can read it or download it HERE. If you would like a hard copy of the first edition used copies can still be found on Amazon.com, Abe books, Thrift books and elsewhere.

Better still, you can avail yourself of the new revised and expanded 2024 edition which I have been working on for almost two years and is almost complete. Eighteen chapters have already been posted and can be freely read or download HERE.

My previous books, as published, may be freely accessed in digital format by clicking the title below.