This is the latest chapter to be published of my new 2024 edition of The End of Money and the Future of Civilization. It provides a comprehensive overview of the alternative exchange movement over the past several decades and its present state, along with important case studies, lessons learned, and prescriptions for significant performance improvements.

Here is a list of section headings with a few brief excerpts:

A currency, to be effective, must be SPENT into circulation. — Thomas H. Greco, Jr

Two Currents of Alternative Exchange

The Tucson Experience

More Recent Experiments in Mutual Credit Clearing

In order for a mutual credit clearing exchange to be scalable and successful over the long run,

-

- The allocation of credit lines cannot be arbitrary but must be based primarily on the value of the goods and services that each participant is prepared to sell within the exchange circle, and,

- The project must be anchored in the local business community, especially the small- and medium-sized enterprises that form the backbone of every local economy and are the providers of people’s everyday needs.

Local Currencies

A Better Currency Model

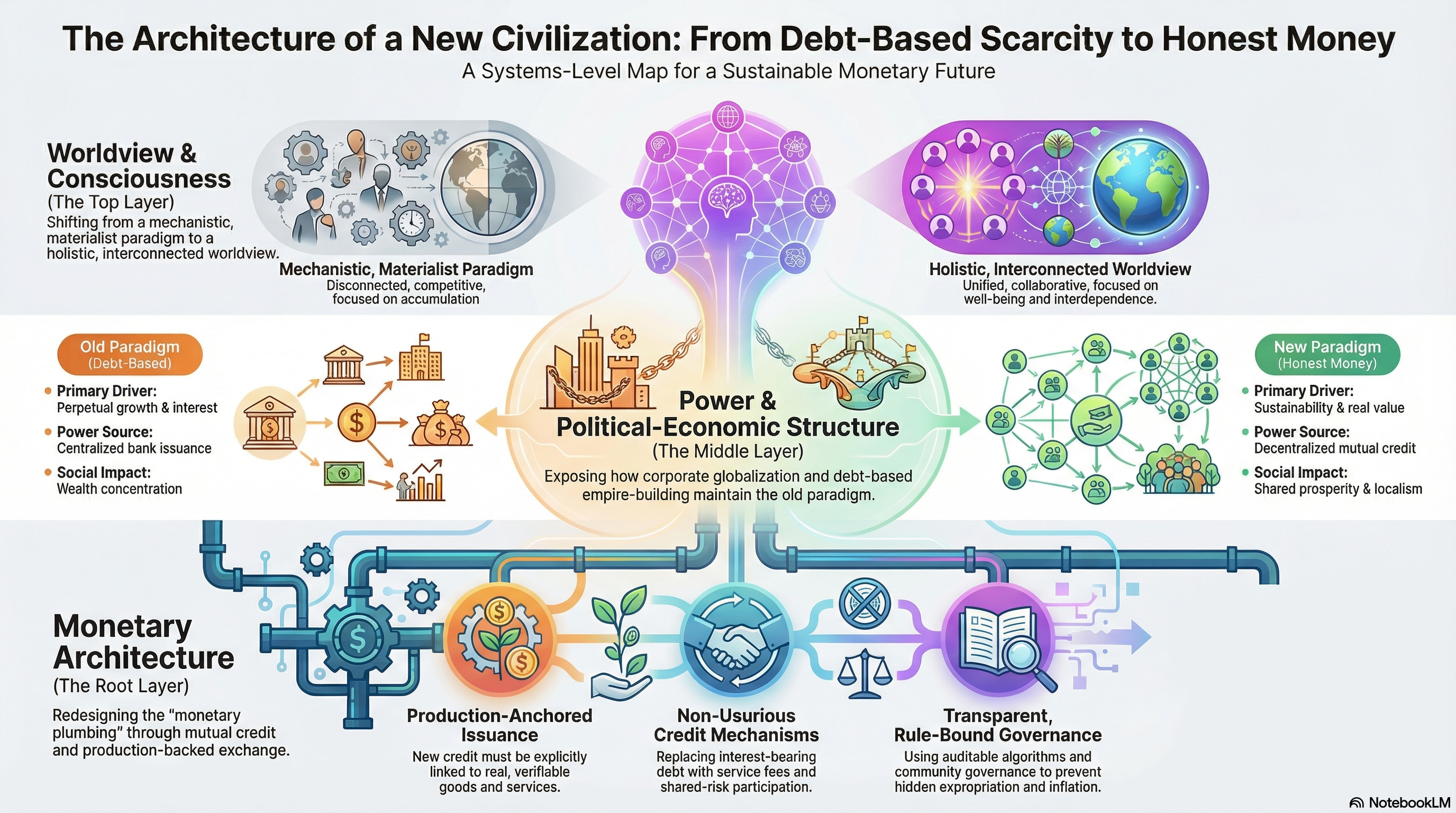

A sound, credible, effective, and scalable currency does not need to be redeemable for conventional money, the issuer needs only to provide credible assurance that its currency can be readily redeemed for some goods or services that are in general demand. Private or community currencies that are SPENT into circulation by trusted issuers, like utility companies, goods producers, or municipal governments, have much greater potential for promoting local community prosperity, resilience, and self-determination because they allow a community to monetize the value that is created and sold by local businesses and professionals. The internal “trade credits” provided to members of mutual credit clearing associations, like those being created by the scores of commercial “barter” exchanges that operate around the world, do the same. Such home-grown sources of liquidity enable a community to greatly reduce its dependence upon official money and bank borrowing, and to automatically favor local production and local sourcing of goods and services, thus reducing dependence upon imports and global corporate providers.

Why Exchange Alternatives Have Failed to Thrive

Case Studies

Prospects for Future Success

You can read the entire chapter at Future Brightly.