In this issue: * Chapter 8—The Separation of Money and State * Upcoming interview on TNT Radio * Six Lessons Learned About Community Currencies * Mutual Credit Panel Discussion * Symbiotic Culture ____________________ Readers have already seen the first two items in the posts below. Here are the remaining three items: ____________________ 6 Lessons Learned from 40 years of experimentation with local and community currencies.

Over the past several decades, many local and community currencies have come, and most of them have gone. By observing all that, and by my own research and experience with Tucson Traders and LETS Sonora, I’ve discovered several fundamental principles that have led me to the prescriptions I have been offering. Here is a partial list:

1. A community currency, to be truly effective, must be more than a local version of the existing political fiat currency. 2. A community currency must be created independently of the banking system. 3. A community currency can be created by local producers of real value in the form of vouchers that they can spend into circulation. 4. The amount of vouchers spent into circulation must not exceed the amount that an issuer is able to redeem by delivering goods and services within a few months’ time. 5. Such voucher currencies may wander away from the local community, but they must eventually return to the community to be redeemed by the issuer. 6. Voucher currencies must have an expiration date or demurrage fee to stimulate a healthy velocity of circulation, and to guarantee their timely redemption.

Zachary Marlow, founder of the Moneyless Society initiative, has recently posted the video of a panel discussion on mutual credit which he hosted several weeks ago. I was one of the panelists, along with Matthew Slater, Dil Green, and Matthew Schutte. You can view it on YouTube. ___________________ Birthing the Symbiotic Age

Here is something that is truly different from the way most of us are accustomed to thinking about positive social, economic, and political change.

Richard Flyer has been working for decades to facilitate the emergence of what he calls a “Symbiotic Culture.” Inspired in large part by his involvement with the Sarvodaya movement in Sri Lanka, Richard has been describing in his new book an “Ancient Blueprint for a New Creation.” The book, which is being published in sections, goes beyond theoretical reasoning or wishful thinking, it is a story or Richard’s journey of discovery and his real-world experience in acting as a catalyst to help that “new creation” to come about. In a recently published section titled, Chapter 7, Part 2, The Conscious Community Network and Local Food Ecosystem,Richard describes how the Northern Nevada Local Food System Network was able to emerge out of his one-on-one conversations with six “super connectors,” showing them how their common interests could be served by connecting their individual “silos” and cooperating for the benefit of all. He reports that, “Through these six people’s networks alone, we expanded the playing field for our food network to almost one hundred organizations and the fifty thousand people they were connected to!” In explaining the success of the network, Richard described it this way:

“A Symbiotic Network is not a separate organization. Instead, it is a community-wide, multi-hub, network-centric ecosystem — really an “organism” — where power is shared by the stakeholders.”

It’s a virtuous, purpose-based network for mutual benefit, where participants ask, “What can I give?” It’s not a fixed coalition where each organization only wants to “get” something.

It’s a unique “umbrella” or “meta-network” designed to enhance the work and provide tangible benefit to each member organization and the whole community – not just another competing silo.

It’s a completely independent network, not controlled by an existing non-profit, business, or local government.

It’s an informal consortium that connects and proliferates the good in a region in one or more multiple domains (e.g., around food, education, health care, neighborhoods, arts and culture)—not a formal organization with a formal board of directors, executive director, CEO, employees, and budget.”

I am confident that if you read or listen to all three sections of his Chapter 7, you will want to go back to the beginning of the book to hear the rest of Richard’s remarkable story. ____________ Wishing you a pleasant summer, Thomas

Covering the history of centralized banking, the danger of today’s concentration of wealth in the hands of a few who are working to completely control humanity; and the need to reinvent money, devolve power to local communities, and create honest “home-grown” means of payment (liquidity). His highly acclaimed book, The End of Money and the Future of Civilization, is being revised, updated, and expanded to reveal how the dysfunctional money system operates, and how to reinvent money to enable the honest exchange of value. New chapters are being posted serially on Future Brightly, on his website, as well as on his Substack and Medium channels. Almost all his writings and accumulated resources for researchers and monetary innovators can be downloaded free at BeyondMoney.net.

You can view or download the video here or on Podbean

The world is governed by very different personages from what is imagined by those who are not behind the scenes. —Benjamin Disraeli, British Prime Minister under Queen Victoria

Chapter Five, the latest chapter in The End of Money and the Future of Civilization, new 2024 edition, is now available. It is being published first on Ken Richings; Substack channel, Future Brightly. Ken has greatly assisted my work in many ways, including editorial assistance and narration of each chapter. He has now posted all previous chapters, and starting now with Chapter 5, each new chapter will appear on his channel two weeks before being posted here on my website or elsewhere. I do not wish to place paywalls between me and my readers so all content will continue to remain freely available to read and download, either from Ken’s site or my own sites but I encourage you to reward Ken for his good work by opting to take a paid subscription to https://futurebrightly.substack.com/.

Chapter 3, The Contest for Rulership—Two Opposing Philosophies. is now available. You can find it on my website, complete with end notes, along with previously published chapters 1 and 2. Click on the links below to access the text and the audio narration. Additional chapters will be posted as they are completed here. I expect to complete Chapter 4 and post it around the end of this year.

As always, your comments and suggestions will be welcomed, Thomas ___________________

Give me the power to create the money and make it legal tender and I can become owner of the entire world. — T. H. Greco, Jr.

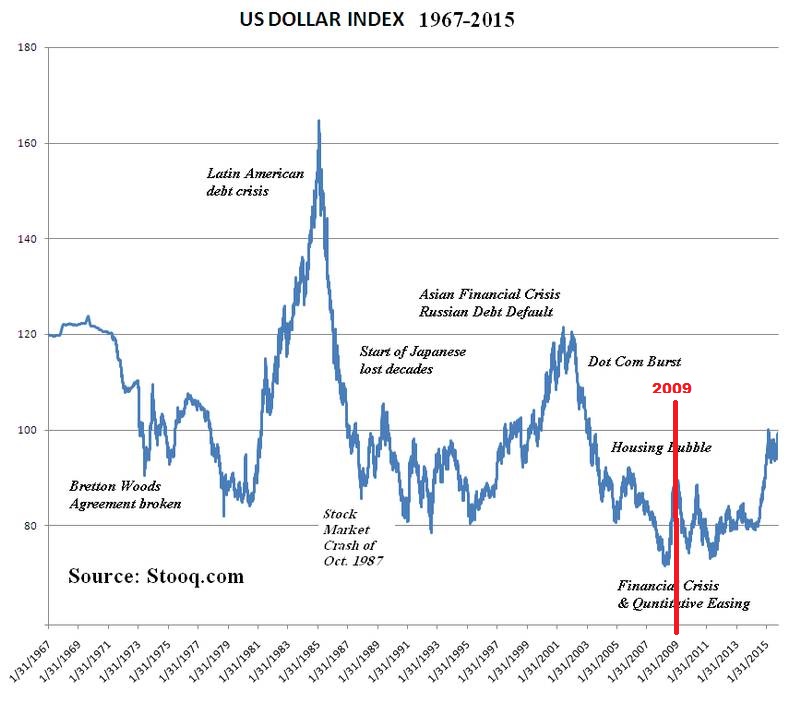

In 2009, while in the process of making the final edits to my book, The End of Money and the Future of Civilization, my editor took issue with my assertion that the declining value of the US dollar would continue indefinitely. He cited the increase in “value” of the dollar in the foreign exchange markets that was occurring at that time as evidence of my “error.”

I responded that the “value” of the dollar compared to other political currencies did not reflect its true value in relation to the real economy, i.e., what a dollar could buy, because all national currencies suffer from the same defects (improper and excessive issuance and the “growth imperative”), and virtually all of them are losing “purchasing power” because of it. The fluctuations in their market values relative to one another result from political and monetary policy decisions taken in their respective countries, not from any increase in their real value.

I argued that what the world has been experiencing in recent years is unprecedented. Never before in recorded human history has there been such a unitary system of money, banking and finance upon which the economies and peoples of virtually every nation of the world have come to depend.

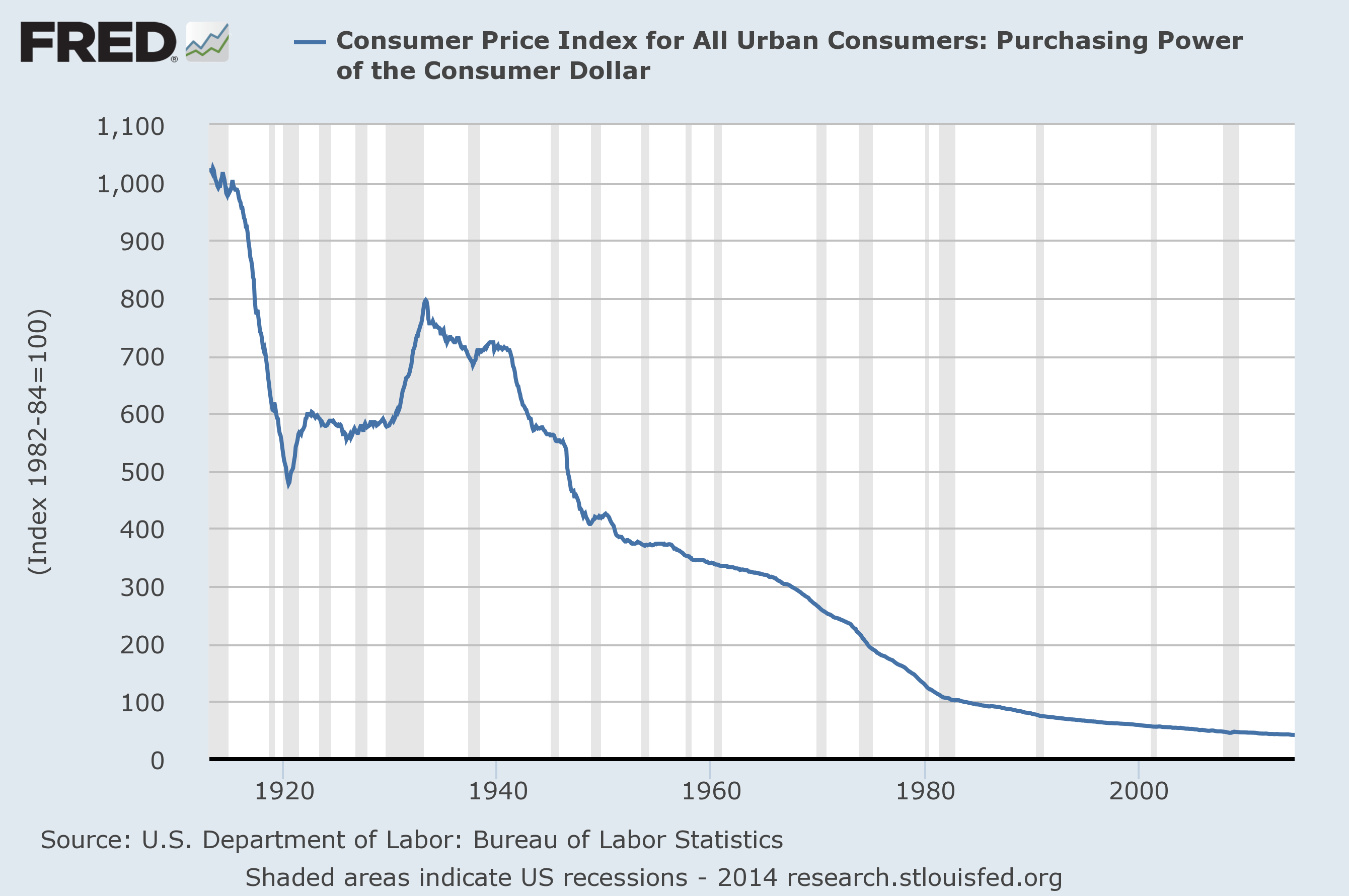

The long-term trends were, and remain, clearly evident and even worse than shown in the above graph. I referred my editor, among other things, to this Max Keiser video to drive home that point and to show that the Consumer Price Index (CPI) is being manipulated to make the decline in purchasing power look less bad than it actually is. Fortunately, that video is still available on YouTube. The mountain of evidence that has been accumulated during the years since the publication of my book has made it patently clear that my assertions were correct. The cost of living due to the debasement of the US dollar has not only continued to increase but has accelerated with the extreme measures that were taken during the pandemic years. Thus, the real value of the dollar, i.e., its purchasing power, has continued to decline even more rapidly than before, as indicated by the recent upturn in the CPI shown in the graph below.

If a strong dollar is in the interests of maintaining confidence and perpetuating the global system, the central banks of the western alliance will rally to support it. If currency inflation is causing prices to rise too rapidly in one place, the effects will be shifted to another place. In efforts to limit inflation overall, the productive sectors of the economy will be starved for credit, causing sound businesses to fail and more jobs to be sacrificed. People who have lost their livelihood are in no position to demand higher wages. Indeed, they will fight with one another to get whatever they can garner from a weakened economy. I argued at the time, and still maintain that the businesses that survive will be the huge corporations that enjoy favored treatment in receiving government bailouts and credit from banks and that those corporations will continue to grow ever larger through acquisitions, consolidations, and market dominance.

Cancer and the Debt Growth Imperative

One of humanity’s most dreaded diseases is cancer, which is tissue growth that has become uncontrolled and purposeless. It is growth of the wrong sort and in the wrong places which eventually kills itself as it kills the body of its host. Such has also been the nature of much of the economic growth that the world economy has experienced over the past many decades.

The debt-growth, economic-growth imperative that I have written so much about and summarized in The Usury Conjecture, can be visualized by thinking of the financial economy as a balloon that is attached to an air tank that is relentlessly filling the balloon with air. If you squeeze the balloon at one point to try to stop its expansion, it will simply bulge out somewhere else. In this analogy the air is debt, and the pressure in the air tank is generated by the interest that is applied to the “loans” that banks make to create fiat debt-money. The ever-growing debt must show up either in the private sector or in the public sector.

Those few who control the interest-based, debt-money regime have historically been given everything they’ve asked for to keep this flawed and destructive system alive. They have amassed enormous financial, economic and political power and are intent on owning and controlling everything. Nothing is sacrosanct; all will be sacrificed on the altar of Mammon because of this Faustian bargain between the money powers and the political powers that was struck centuries ago.

But despite the powerful tools at their disposal, they cannot forever avoid the inevitable. As the long-term negative trends continue and the symptoms become ever more severe, the people, communities, and independent producers who are adversely affected will get serious about rediscovering and inventing ways to escape. They will deploy their own honest and effective means of exchange and finance that will ultimately displace the old dysfunctional and destructive political system of money and finance.

Fortunately, the honest and effective systems of exchange and finance that I’ve long been describing in my books, The End of Money and the Future of Civilization, and Money: Understanding and Creating Alternatives to Legal Tender, are already available and are being employed at the margins of the economy. While their scale of operation is still relatively modest, it is inevitable that as improvements are made and their necessity becomes ever more evident, efforts to decouple from the dominant monetary and financial regime will continue to intensify, money banking and finance will be reinvented, and the chaos that now reigns will give way to a better world for all.

The US dollar is rapidly losing its status as the global “reserve currency.” One after another, nations outside of the western coalition are waking up to the fact that dollars are needed only to pay for imports that come from the United States. In trades with other countries they are choosing to begin paying one another by using their own currencies, as reported in videos like this. They are recognizing that the real resources that they own are much more valuable than the empty promises that are embodied in inflated US dollars or other political currencies. The exploitation of weaker nations by the western powers that has been ongoing for centuries is coming to an end and the emergence of a multi-polar world order is now unstoppable.

The Bretton Woods agreement that established the post-war world financial order in 1944 was based on the promise that US dollars would be redeemed for gold at $35 an ounce. But the continuous debasement of the dollar over the years made that completely unrealistic, and ultimately its impossibility was formally recognized when President Nixon in 1971 “closed the gold window” and announced that the US government was reneging on that commitment. It would no longer give gold for dollars except at the prevailing market price. From that point on the fate of the dollar was sealed; it was just a matter of time. Despite the imposition of a series of extreme financial, economic, political, and military measures by the US and its western allies, time has run out on dollar dominance and the unipolar world order.

The main questions now are, 1) to what further extremes will the western empire resort in its desperate effort to forestall the inevitable political reordering, and 2) what sorts of new monetary and financial arrangements will be established to supplant the old Bretton Woods arrangement?

Regarding the first of these, the past several decades have seen a succession of both covert and overt interferences designed to weaken or neutralize monetary dissidents and potential political and economic rivals. Notable among the former have been Saddam Hussein, who in 2000 began selling Iraqi oil for Euros instead of dollars, and Muammar Gaddafi the Libyan leader who had plans to launch a pan-African currency called the Gold Dinar to free Africa from American domination. As a consequence, both men were murdered and their countries destroyed. Following the NATO invasion of Libya, and the murder of Gaddafi, then Secretary of State, Hillary Clinton, disgustingly and arrogantly boasted, “We came, we saw, he died!”

But nuclear armed Russia and China are not so easy to push around and brought to heel. When their Russian puppet Boris Yeltsin chose Vladimir Putin to succeed him as prime minister, the globalist western oligarchs thought they could continue to rape Russia and exploit its vast resources for their own purposes. But Putin surprised them with his loyalty to “Mother Russia” and his unwillingness to betray the Russian people to the globalists. Whatever we in the west might think about the man, his stance has clearly endeared him to the Russian people.

When the Soviet Union collapsed, the western powers promised not to move NATO farther to the east, but they have reneged on that promise, and one by one have brought the former Soviet republics into the western fold. [Robert F. Kennedy Jr. has elaborated on this point in his recent speech and highlighted the importance of respect for Russia’s legitimate security concerns if ever there is to be peace]. Then, in 2014 the CIA engineered the overthrow of the elected government in Ukraine and replaced it with their own puppet government to further pressure the Russian government to play ball. The perceived existential threat of NATO weapons, even nuclear ones, on their very doorstep, was too much for Russia’s leadership to bear. It should have come as no surprise to anyone that the Russians reacted as they did to counter that threat by launching their “special military operation.” Putin had stated repeatedly that he hoped to negotiate a deal that would respect Russia’s national security interests but the US government has chosen to perpetuate the war in order to weaken Russia and force it to submit. Former nuclear weapons inspector, Scott Ritter, with his military experience and vast knowledge of the region provides a much more nuanced picture of that siltation than the biased sound bites one typically gets from the mainstream media.

Farther to the east, China a major economic, political and military power, has also balked at submitting to a New World Order in which the Western Empire calls all the shots. So now the globalist oligarchs who control the US government see China as a major obstacle to their plan for establishing a trans-human, technocratic utopia under the control of the elite Super Class. Hence, we see continual saber rattling, military and political provocations, and endless prating about the “Chinese threat.”

Regarding a new system of exchange and finance, I expect that we may soon see the emergence of a multilateral system for clearing credits among nations, one that will be more along the lines of the Bancor plan that John Maynard Keynes proposed at Bretton Woods in 1944. Not that Keynes should be the last word on the matter, but he at least proposed a way of preventing trade deficits from becoming perpetual as they are now, by imposing a levy (interest) on positive balances, as well as negative balances, that would seem to eliminate the debt trap. Professor Perry Mehrling provides a brief description of the Bancor plan in this video.

I expect eventually to see the complete depoliticisation of money and the broader application of credit clearing directly among buyers and sellers at the level of individual traders, as they have been doing for decades through the scores of commercial trade exchanges that have been operating around the world. Money is, after all, merely an information system about credits and debits that enables goods and services that are sold to pay for other goods and services that are bought. Further, the settlement of accounts will be done not only through reciprocal exchange, but also through cooperative support and forgiveness of debts, which will bring with it greater fairness and finally a peaceful world. Indeed, there may someday be a world government, but it will not be imposed by force, nor will it be the product of greed and materialistic human minds.

# # #

Addendum: In this excellent article, America Has Just Destroyed a Great Empire, Prof. Michael Hudson offers a history lesson that underlines the points I’ve made in my article.

Here is a small excerpt:

Having endowed the region’s cosmopolitan Temple of Delphi with substantial silver and gold, Croesus asked its Oracle whether he would be successful in the conquest that he had planned. The Pythia priestess answered: “If you go to war against Persia, you will destroy a great empire.”

Croesus therefore set out to attack Persia c. 547 BC. Marching eastward, he attacked Persia’s vassal-state Phrygia. Cyrus mounted a Special Military Operation to drive Croesus back, defeating Croesus’s army, capturing him and taking the opportunity to seize Lydia’s gold to introduce his own Persian gold coinage. So Croesus did indeed destroy a great empire, but it was his own.

Fast-forward to today’s drive by the Biden administration to extend American military power against Russia and, behind it, China. The president asked for advice from today’s analogue to antiquity’s Delphi oracle: the CIA and its allied think tanks. Instead of warning against hubris, they encouraged the neocon dream that attacking Russia and China would consolidate U.S. control of the world economy, achieving the End of History.

But that’s not the way it’s working out. Please read the full article.

What You Need to Know About Money. Currency, Credit, and Exchange

Abstract: There remains today, even among economists and “experts,” a general lack of understanding about the essential nature of money, currency and credit, and sound principles of their creation and management. This article provides a point-by-point summary of fundamental concepts and basic principles of exchange, it outlines the systemic defects and destructive nature of the dominant political, central banking, interest-based, debt-money system, and describes the ways in which honest and effective exchange media can be created on a decentralized basis outside of the banking system and in lieu of political money. A wider understanding of these points will lead to the widespread creation of honest exchange mechanisms and the devolution of financial, economic and political power that can change the course of civilization from self-destruction toward peace, justice, freedom and harmonious relationships.

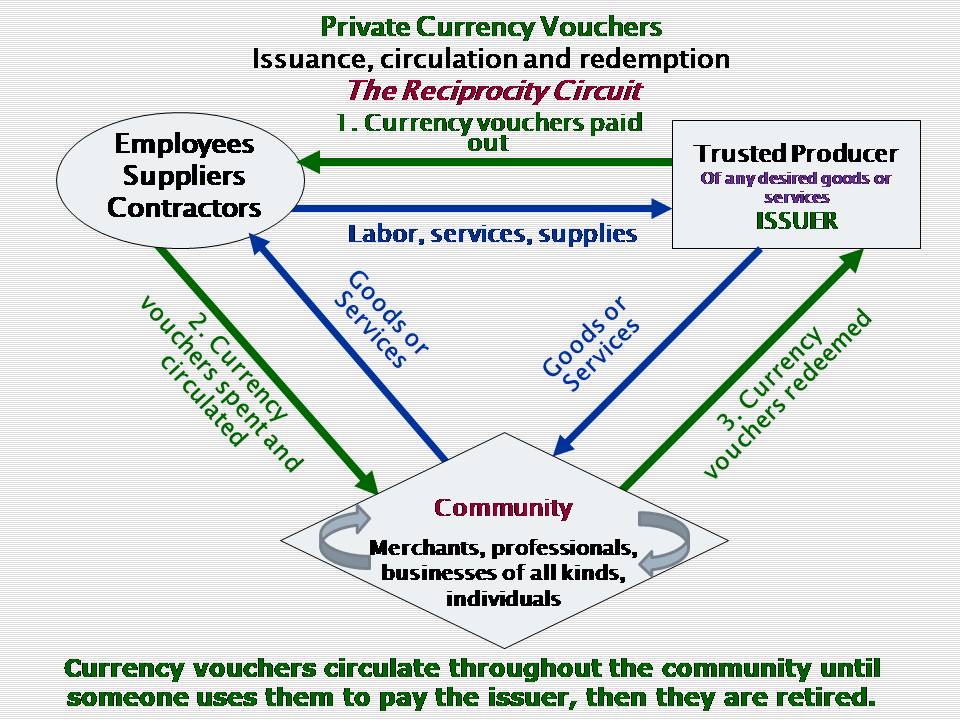

The essential nature of money/currency A currency is a credit instrument, i.e., a promise to deliver valuable goods and/or services.

Basis of Issue A currency must therefore be issued into circulation on the basis of some value foundation, i.e., goods and/or services that the issuer is ready, willing, and able to sell immediately or in the near future.

Purpose of a currency The sole purpose of a currency is to facilitate the reciprocal exchange of value in the market. It is not a measure of value, nor is it a savings medium.

Reciprocal Exchange Reciprocal exchange is the voluntary exchange of one sort of value for another in the market.

Issuance A currency enters into circulation when a provider of value offers it to another seller who accepts it as payment for their own goods or services, i.e., it is spent into circulation, not sold for fiat political money.

Circulation If it is to serve as a currency, a credit instrument must circulate freely and can change hands many times before eventually returning to the issuer for redemption, not for political money, but for the goods or services that are the issuer’s stock in trade.

Redemption and Extinction A currency is redeemed and extinguished when the reciprocity circuit has been closed, i.e., when the issuer accepts it back as payment for the goods and/or services that they are prepared to deliver immediately or in the near term.

Liquidity Liquidity is quite simply the ability to pay, i.e., having a payment medium that is widely accepted.

Monetization Monetization is the process of converting the value of an illiquid asset into a liquid form, i.e., a form that can be used as a payment medium (money/currency).

Who is qualified to issue a currency? Since a currency is a promise to deliver value, only producers and providers of real value are qualified to issue a currency.

Fallacious myths about money

The belief that money must be issued and controlled by governments and/or central banks.

The belief that banks collectively should have a monopoly on the allocation of credit.

The belief that interest is a necessary element in money creation and finance. How is conventional political money issued, and who issues it?

Virtually all political fiat monies are created by banks when they grant loans.

What are the flaws in political money system, and what are their impacts?

Most bank loans are made on an improper, or inadequate, basis or foundation.

Government and central bank currencies are no longer defined in terms of any real concrete value unit.

Thus, most political money is illegitimate and dishonest.

The interest that banks charge on loans far exceeds the cost of providing the service of monetizing the value of the collateral assets. This causes debts in the aggregate to grow exponentially over time making it impossible for all borrowers to repay what they owe, and making it certain that some must fail.

The concentration of money power in the hands of ever larger banks, in collusion with central governments, concentrates financial, economic and political power in the hands of an elite “super class” and undermines democratic government.

Assertions and Prescriptions

To preserve any semblance of social justice, economic equity, individual freedom, and democratic government, power must devolve to people in their various communities. The only feasible way of achieving that is through the creation of independent and honest mechanisms for exchanging value.

Such honest mechanisms include private currencies issued by providers of real value, and credit clearing associations that allocate credit on a sound basis to producers of real value, and enable them to exchange value without reliance on bank borrowing or the use of political money.

Such systems are not new; they have long existed and need only to be optimized, standardized, and networked together to provide means of exchange that are locally controlled yet globally useful.

The future will see the proliferation of entities that organize and enable the allocation of interest-free exchange credit to small- and medium-sized enterprises (SMEs) that are the backbone of resilient and sustainable community economies.

Standard procedures and protocols for credit allocation and management will emerge that will allow the effective networking of those entities into a global “internet of exchange” using credit that is locally controlled but globally useful.

____________________________ The Emerging New Civilization

Is our civilization collapsing? If so, what can be done about it? Can it still somehow be saved? If, not, what will be the impact on people in various places and cultures? What sorts of new systems and structures will emerge to take the place of the old?

These are some of the questions that my longtime friend and correspondent, Prof. Jem Bendell, addresses in his new book titled, BREAKING TOGETHER – a freedom-loving response to collapse. Having received and read an advance copy, I’ve been deeply impressed with the depth of Jem’s research and clarity of vision, and moved by his personal story of mind-change and commitment to advancing the common good. Far from doom and gloom, the message of this book is hopeful and inspiring.

In his introductory chapter, Recognising and Responding to Collapse, Prof. Bendell addresses these topics:

Finding our bearings in a world that’s lost

What is collapsing?

Why is this perspective not widely known?

Allowing the emotion of it all

From repentance to radicalization

Freedom from the failing of fables

Freeing humanity to our true nature

Breaking together

I strongly recommend that you listen to a reading of that chapter at SoundCloud. For information on purchasing Prof. Bendell’s, book, or to receive a free copy as an e-book, go to his website.

“Backlash against the COVID-19 fiasco of the last three years is building among a public that is slowly waking up to the unprecedented power grab and wealth transfer that took place under cover of a pandemic.”

“Can a coalition be built in a divided and suffering population to combat the political and economic nexus — namely the corrupt merger of state and corporate power — that is ruining the health of the people and the planet, and trampling our rights and freedoms in the process?”

“He (Prof. Jem Bendell) writes (in his new book, Breaking Together) that “climate concern is being highjacked by a mix of corporate profiteers and authoritarians, so that ineffective and counterproductive policies are being implemented and thereby generating a backlash against any kind of concerted action.”

His proposed solution is to reboot environmentalism into an “eco-libertarian” movement that seeks to protect both our freedoms and the environment from big corporations, corrupt governments and Davos elites.”

“In the overlap between the Left and Right versions of the popular revolt against the corrupt merger of state and corporate power, laid bare by the glaring abuses of the COVID-19 era, there may be room for unexpected political bedfellows to build a broad-based movement that appeals to significant segments of the electorate.”

Indeed, I’ve been seeing the emergence of what may become “a new grassroots populist majority that transcends the old boundaries of left, right, and green, liberal and conservative, rural and urban.” If we are to save democracy, the environment, and our very humanity, and build a just and equitable “new civilization,” we must overcome our knee-jerk reactions, listen deeply to each other, look at all the evidence, and build new alliances that transcend old labels and political rivalries. ____________________________ Fifth generation warfare and Sovereignty

“Fifth generation warfare is a war of information and perception,” and you are the enemy. In his excellent presentation, Dr. Robert Malone outlines the strategies, tactics, and technologies that are being used by “the national security state” to manipulate people’s emotions, and shape our thoughts, attitudes, values, and beliefs. He states that, “In fifth generation warfare your mind is the battleground,” and gives us guidance on how we can shield ourselves and ultimately win.

In this interview, Robert F. Kennedy Jr. recounts some essential history of his uncle’s Presidency, including his continuous battle with and the CIA and “the military-industrial complex” that President Eisenhower warned us against. Kennedy says flatly that “…the case against the CIA in the assassination of my uncle is beyond a reasonable doubt.” You can view a one minute video of his assertion from the New York Post.

The Most Dangerous Man in America is a documentary film about Daniel Ellsberg and the Pentagon Papers. I first viewed it prior to its release in 2009 and then, a few days ago I got together with some friends and watched it again (on Kanopy). In light of what has transpired in the interim, it seems even more important now for people to be aware of it and grasp the significance of its message. In this interview with The Guardian (UK), looking back 50 years, Ellsberg says, “I’ve never regretted doing it.”

“The man who exposed US lies about the Vietnam war says the culture of official secrecy is worse today. But he urges whistleblowers: ‘Don’t wait years till the bombs are falling and people have been dying’”

____________________________ My Recent Interviews and Posts

In this interview I provide a succinct description of the present central banking, interest-based, debt money system and its dysfunctional nature, the global crisis that it has resulted from it, and what we can do to transcend it.

In this conversation we discuss our collective predicament and what people are doing to preserve our freedoms, assert our rights, and build a better world.

This post will be of particular interest both to monetary and economic researchers, and to practitioners. It describes my sizable and unique collection of books, pamphlets and other print materials, many of which are available in digital format, and announces a couple important additions, specifically, Ralph Borsodi’s, Inflation is Coming and What to Do About It, and, Hugo Bilgram’s, A Study of the Money Question.

____________________________ Finally, I have agreed to present at an Anti-authoritarian gathering in Switzerland on the 21st of July. I will most likely participate remotely to avoid depleting my strength with a long intercontinental journey. The gathering is billed as Anarchy 2023, but don’t be put off by that label. Oligarchs and despots have sullied the word “anarchy” by equating it with chaos, but the true meaning of the word “anarchy” is “without rulers,” it raises the question of the true locus of sovereignty and seeks the empowerment of people instead of kings, emperors, presidents and “representatives” that inevitably become repressive and tyrannical.

This post is adapted from a conversation I had with one of my followers in 2021. The questions that were posed are quite pertinent and wide ranging, and I think my answers will be of interest to anyone who wants to understand mutual credit clearing and/or is considering designing and implementing one.

1. At the least minimum, how many businesses should be there in the network to begin tradingwith each other and should we be thinking about a maximum limit, if yes, then why and how?

It is not only a matter of numbers but also of variety of goods and services represented and the volume of sales. Conceivably, a mutual credit clearing network could begin with a single large trusted business that would have a large line of credit in proportion to their monthly sales volume, say a debit limit of 2 or 3 times monthly sales. All other members would need to earn credits before they could spend credits, they would have no line of credit until they had demonstrated their earning capacity within the network. But it would be better in many ways to have a number of “trusted issuers” who offer a variety of goods and/or services that are in regular demand, and who thus qualify to receive a line of credit.

In practice, commercial trade exchanges do not launch until they have a few hundred members that offer diverse goods and services, but in each case, the line of credit (debit limit) must be proportionate to their capacity to provide desired goods and services.

2. What are the differences in benefits for an issuing member, non issuing member?

An issuing member has been given a line of credit; they can spend before they earn. A non-issuing member does not (initially) have a line of credit; they must earn credits before they can spend credits. As they demonstrate their capacity to sell as well as buy, they may then qualify for a line of credit.

3. How can a non member of the network be a part of it?

A non-member can join the network to buy from, and sell to, the other members. Also, a non-member can be brought into the process by accepting vouchers issued by the network, as follows: It a member wishes to buy something from a non-member, s/he might ask the network administration to create voucher notes or tokens which they can draw against their account balance or line of credit. Those vouchers can then be offered as payment to a non-member vendor for goods or services. If the non-member is willing to accept them, the vouchers could then circulate outside of the network, but the voucher must have an expiration date to assure that the credits they represent will be returned to the network ledger when they are used to buy something from a network member.

4. In India, we have a savings culture as most people are still conservative when it comes to their money and also because there are major future investments for parents and families because culturally they are responsible for getting their children educated and married both requiring a lot of money. In that context, won’t people be uncomfortable in having just a medium of exchange and not able to save the currency which is a general tendency.

Surely, people need to save, and there are many ways to do that already. Savings can take the form of real assets, like precious metals, collectibles, tools, equipment, land, buildings, machinery, etc., or financial assets like corporate shares, bonds, savings deposits at a bank, etc.

Those ways remain available and assets can be acquired with an alternative currency as well as with conventional currency from anyone willing to accept the alternative currency in exchange for those assets. In the early stages, it is more likely that an alternative currency will be accepted for real assets than for financial assets, most of which must be acquired from banks and other institutions that are part of the dominant fiat money system. As I’ve suggested in my books, as a credit clearing exchange develops it can add savings mechanisms to it exchange services. Those who have surplus credit balances can shift them to their “savings” account just as people do now by shifting balances from their checking account to their savings account at their bank or credit union.

5. When the network reaches different sizes of member businesses like 20, 50, 100, 500, 1000: In these instances, how should the credit allocation be thought about, will it change according to the size or the types of businesses in the network, how to decide what number of possible issuers can issue at one time meaning how to think about the maximum credit issuance in a network?

I’m not sure what you’re asking here. The overall amount of credit that exists within a network at any one time will adjust itself according to the amount needed to complete all desired trades so long as account balances remain within allowed limits. Each account will be evaluated individually to decide its debit limit by applying a standard algorithm that is based mainly upon the sales volume of that account but also may include other factors such as the type of goods and services it provides (essential necessities that are in constant demand, or not), reputation with customers and/or suppliers, overall indebtedness (and risk of insolvency), sales trends, etc.

It is expected that most account balances will remain well within allowable limits but still provide the members with adequate liquidity. Those that are chronically close to their limit will be assisted in finding new customers and sales possibilities and/or developing new products and services that are in demand.

6. In India, in the informal sector (which is minimum around 60%), a transaction happens either fully in cash or partly in cash (not shown in records for tax purposes) and partly cheque/ bank transfer/ net banking etc. What needs to be done in such a scenario?

Under the present circumstances, government policies are typically antagonistic towards small and micro-businesses, and support market dominance by large corporations. It is hard to fault anyone for trying to avoid tax liabilities by using paper cash and other anonymous payment options. But the evident recent trend has been toward the elimination of cash by governments. Governments and banks everywhere seem determined to force a shift of monetary and financial transactions onto channels that allow every transaction to be tracked, and upon which taxes and fees can be levied. Furthermore, the complete replacement of cash by such digital currency systems will further tighten government control over how you spend your money, or whether you will be allowed to access it at all.

Mutual credit clearing is not intended to be a means for avoiding taxes. Rather it is a way of providing an economy with liquidity (a means of payment) that is independent of the banking system and supplemental to the supply of political money. See my web post, There ain’t no such thing as a free lunch: Principles of Credit, Exchange, and Finance, especially Addendum 2.

It is crucial to personal freedom, the survival of small businesses, and to local self-determination that such independent payment systems be established and reach significant scale prior to the complete centralization of money power into the hands of the political, banking and corporate elite.

7. Also in our informal sector, we have a data problem because most businesses are not incorporated hence most of them don’t maintain balance sheets which are public and can be trustworthy (again one problem being that they don’t want to show their actual income in order to avoid high taxes), so in that case how do we as an exchange operator could trust the issuing members?

The crux of organizing a system to provide the exchange function is for actors in the economy, be they unincorporated businesses, corporations, or individuals, is in deciding whom or what to trust with a line of credit, and to what extent (how much credit). There are numerous factors that might be considered in deciding credit lines. Each commercial trade exchange has its own system for doing this. Here below is one example. I’m not saying that it is the “right” formula but it serves as an example of a few factors that might be considered. Of course, local circumstances must ultimately be considered in deciding which factors to include and how much weight should be given to each. In the circumstances you describe, reliance will likely need to be primarily upon the reputation a business has among its suppliers and customers, and estimates of business volume based on self-reporting and confirmed by observations. Along with establishing the mechanisms for facilitating the exchange of value, we need to be building communities based on face-to-face interactions and personal knowledge of those we are doing business with.

Recent scandals have show that even the audited balance sheets of public corporations may not be trustworthy.

8. With the issuing principle, you explain in what quantity a business should issue its currency, but just to be sure, does that factor in the sales the business will have in rupees/dollars because that depends completely on the market demand.

At the beginning of operations of a mutual credit clearing exchange, there will be no available data on the volume of sales within the exchange, so one must estimate that potential based upon a member’s sales volume in the rupee or dollar economy, AND the number and size of those exchange members who might be their customers.

9. Will the mutual credit achieve its vision if a transaction is done partly through mutual credits and the rest through fiat (This I think will help people adopt the system because that way they might save in their own currency too and feel safe about it). How should we view this whether part payments will take us to the vision or no?

What you are referring to is called in the commercial trade exchange industry a “blended trade.” This is generally allowed on large transactions but discouraged on smaller transactions. Yes, members may feel more comfortable with blended trades, considering that they need to be sure of covering their cash costs, but it is a departure from the ideal. While a business must cover cash costs overall, cash costs need not be covered on each and every transaction. I recommend that, except on very large transaction amounts, the cash portion should never exceed 50% of the transaction amount. Sardex has used a sliding scale for the percentage of cash allowed according to the size of the transaction.

10. You said to recruit all members of the supply chain till the basic commodity producers, but the supply chain is not just national but international so in that case it looks very difficult until we have credit exchanges all over the world. I understood pretty much I think your regional economic development plan but for so many of the products which just can’t be import replaced, how will the development plan work?

Yes, of course that is the problem; the entire supply chain is not entirely local or even national. But it is important to drill down into the supply chain as far as possible to maximize the amount of transactions that can be cleared. Further, sustainable economics and community independence require that more goods and services be sourced closer to home. The present global economy has extended international trade far beyond the amount that is necessary or desirable, has favoured mega-corporations and industrial agriculture, is dependent upon the subsides and other support provided by national governments and the banking system, is wasteful of energy required to transport goods long distances, and is, in real terms, unsustainable. The necessary transition back toward local production for local consumption requires “import substitution” which works in harmony with, and is stimulated by, the local control of credit and systems of mutual credit clearing.

We must begin with what is presently possible and build upon that. Ultimately, I envision the development of a global credit clearing network comprised of relatively small local nodes — an “internet of exchange” in which credit is locally controlled and managed, but globally useful for payments.

11. Since the taxes are collected by the central government, how will taxation be affected because the central government would never accept it?

Of course, taxes must be paid in whatever currency the government demands, so every member must make sure that they earn enough in that currency to do so.

12. Will the issuers of the currency have the entire line of credit at once in the beginning itself? Or will it be slowly increased?

No, a line of credit is simply a maximum amount that can be accessed, i.e., the limit on one’s debit balance. Trade Credits in a mutual credit clearing circle can be thought as an internal currency. That currency is created only when it is spent into circulation. Prior to that it does not exist; it is not on the ledger. That is also true for conventional money that banks create by making “loans,” but banks pretend that money is a thing so they charge interest on the entire amount of a “loan” even if it remains a deposit in the borrower’s account and never gets spent.

13. Can’t businesses which don’t have regular demand for their products issue currency?

Imagine such a business that does not have a regular demand for their products asking you to accept their private currency as payment for something you are selling. Would you accept it? Why? Would you be able to spend it? Where?

A currency is created when the issuer spends it. What gives a currency value is the issuer’s promise to accept it back as payment for something they sell. If no one wants what they sell, no one will want their currency; it will have no value to anyone. An issuer of a currency must be ready, willing, and able to redeem their currency, not by giving fiat money for it, but by delivering the goods or services they have to sell.

14. How will the network work if there are no issuers and hence no lines of credit for any business to begin with and let’s say there are 20 diverse businesses in that network, the money gets created the moment there’s a transaction between a buyer and a seller as debit and credit in the system and likewise further, what are the effects of it?

It can’t. Some businesses must be assigned lines of credit, i.e., they must be authorized to spend before they earn. The total of debits (or credits) in a clearing system are the “money supply” of the system. No credit; no money/currency.

15. Can the currency be created based on a specific problem a small business faces, e.g., working capital shortage, or increasing employees’ salaries or a specific sector for that matter?

A currency is intended to facilitate the exchange of goods and services; it must therefore be created on the basis of existing goods and available services. A currency thus monetizes working capital (inventories and accounts receivable). Capital improvements, on the other hand, should not be the basis for currency creation because the goods and services that they are intended to produce will not be available until some later time, if at all. Investments in capital improvements must be financed out of savings.

16. In the beginning, should every business get a positive credit allocation regardless if it’s an issuing or a non issuing business?

An issuing business is, by definition, one that qualifies for a line of credit. The qualifications for a line of credit have already been discussed. Please note that in assigning lines of credit there are no judgements being made about anyone’s “personal” worth, but only about the value of the goods and services they offer to sell and the potential demand for their goods and services in the market. The line of credit monetizes the value of those goods and services in the form of trade credits that can be used to make payments to others within the system. Have a look at my monograph that explains that further, Liquidity and Monetization. This monograph defines key terms in the design and issuance of exchange media.

17. Continuing on the supply chain example given earlier, let’s say if a business has 50 SKU’S, out of those, for 20 SKU’S, the suppliers are locally available so there are dealings done with them, but not for the remaining 30, in that case should he keep different numbers for different products? Same goes for products with different margins: How will the business set the credit amount for each product in that case?

An SKU is an identifier of a particular product. Your hypothetical example says that a particular business needs to inventory 50 different items, of which only 20 can be sourced locally. I see no reason why different SKU numbers would need to be used. Those items that are available locally can potentially be paid for using trade credits, while those that are not will continue to be bought using the government fiat currency. The margin on each SKU item is not relevant.

Regarding the second part of your question, I presume you are speaking here again of blended trades. The business will need to work that out based on their experience. As I said before, cash costs do not need to be covered for each individual transaction but must be covered in the aggregate. This leaves room for the business to decide the cash proportion on the basis of marketing and demand considerations as well as financial ones.

18. Is it really right for us to charge the transaction fee on their money? And I couldn’t understand the brokerage fees and other ways of monetizing the service? This question of the business model has me bothering since sometime now both from the ethical and the practical standpoint.

A trade exchange, like any other business, will continue for some time to have some expenses that require cash payment, e.g., for taxes and goods and services that are not available within the trade exchange. Like every other business, it must therefore generate some cash income. As trade exchange networks grow, a larger proportion of the administrative needs can be sourced from the membership using trade credits and the cash needs will decline, then most of the revenues can be collected in trade credits.

19. If a business accepts partially in mutual credit, will the businesses decide how much % that would be and keep fluctuating it according to their needs, and if so, how will it affect other businesses?

Each trade exchange has their own policies about blended trades and, as I mentioned above, there are competitive considerations to be taken into account as well as the overall benefits of the credit clearing services. Businesses should be allowed to vary the cash percentage according to their needs but within certain limits specified in the membership agreement. See my model membership agreement as a possible starting point.

The IRTA has, over the years, produced many policy recommendations for its member trade exchanges and many of its documents are available to the general public. I would recommend that you search their website.

20. You didn’t mention the maximum limit on numbers of businesses in one network?

That number will need to be determined in practice, with due regard to the need to maintain the personal aspect and high level of trust among the members in each local exchange circle (node), and the “Dunbar number” or “Rule of 150.” Here’s an excellent article that explores the question: Dunbar’s number: Why we can only maintain 150 relationships.

21. How will an issuing business actually ever know how much to issue because he will never know how much business is going to come through fiat money meaning how much inventory will he order?

An issuing member issues currency by buying from others in the circle, or in the wider network of circles. He is then committed to sell that same amount of value in return for the trade credits he issued. If trade credits are presented as payment he must accept them so long as he has credits outstanding (a negative balance on his account). He must have sufficient inventories to satisfy the total demand regardless of the form of payment tendered. Since his credit line was assigned on the basis of his likely sales, there should generally be no problem about his ability to deliver. Actual performance of each account must be monitored and action taken to prevent problems from developing.

22. How will the network adjust itself, as you mentioned in the document earlier? Are there real world examples on that?

I said the “volume of outstanding credit” will adjust itself. If there is very little buying and selling within the trade exchange then there will be very little credit on the books; as more trading occurs, more credits will (potentially) be created.

23. What do you mean by “businesses remaining well within allowable limits”?

Just what I said, “Each account will be evaluated individually to decide its debit limit by applying a standard algorithm that is based mainly upon the sales volume of that account but also may include other facts such as the type of goods and services it provides, reputation with customers and/or suppliers, overall indebtedness, sales trends, etc.”

24. What software platforms are available to use right away at low cost or even for free? How do i get started as quickly as possible with the software?

That depends upon the level of security you need. There are many proprietary programs available in the commercial trade exchange sector.

A few free options that I’m aware of include: Cyclos (https://www.cyclos.org/products/). Version 3 is open source and free, while version 4 is free to try and more functional.

Community Exchange Network (CES) (https://www.community-exchange.org/home/) is a platform that provides free hosting for hundreds of local currencies and exchange systems worldwide.

Community Forge (https://www.communityforge.net/en). “Community Forge is a non-profit organization that designs, develops and distributes tools around complementary currencies.”

25. What are brokerage fees?

Commercial trade exchanges typically employ brokers to assist users in finding both sales opportunities and ways to spend their trade credits. Usually, these services are included in the membership fees, but brokerage services may be billed separately.

26. Are there contextual factors you think should be understood before implementation?

Yes, launching a mutual credit exchange requires a lot of ground work in making contact with prospective participants, getting expressions of interest, and ultimately commitments to participate. It is helpful to work through established networks like business, social, cultural, and religious organizations. Publicity and news articles can help with recruitment and generation of a favorable attitude among the general community.

In this conversation we discuss our collective predicament and what people are doing to preserve our freedoms, assert our rights, and build a better world.

The first edition of my book, The End of Money and the Future of Civilization, was published by Chelsea Green Publishing in 2009. While it remains as relevant today as it was when first published the printed book has been out of print for several years. But, having had the rights reverted to me by my publisher, I am making the entire book available for free in PDF format. You can read it or download it HERE. If you would like a hard copy of the first edition used copies can still be found on Amazon.com, Abe books, Thrift books and elsewhere.

Better still, you can avail yourself of the new revised and expanded 2024 edition which I have been working on for almost two years and is almost complete. Eighteen chapters have already been posted and can be freely read or download HERE.

My previous books, as published, may be freely accessed in digital format by clicking the title below.